Although uncertainty about Social Security benefits may not be present in all surveys, it is much higher among younger people. The Survey of Economic Expectations includes a Social Security section. The researchers obtained six points as well as a minimum and maximal value for a subjective probability distribution. The researchers derived measures of uncertainty for each respondent. It was clear that younger respondents were less certain about their future benefits. They were also anxious about the Social Security program as a whole.

Pessimism

Recent surveys have indicated that most Americans are not optimistic about their prospects for collecting Social Security benefits when they retire. Pessimism seems to be most prevalent among Americans aged 18 to 29 years. However, the general population is just as susceptible to this outlook. Nearly half of people aged between thirty-four- and fifty-nine do not expect to receive any Social Security benefits when they retire.

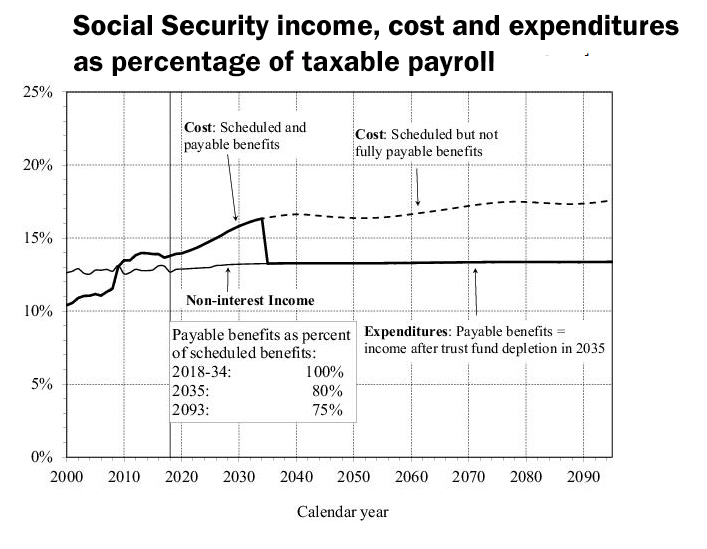

According to a recent report, Social Security will have to cut benefits for those who pay payroll taxes by 2034. Social security benefits are likely to be cut by close to 25% if Congress doesn’t intervene. The government will have to raise the payroll tax in order to pay the deficit. If the trust fund was exhausted in 2035, the amount of benefits available to retirees would decline by 25 percent.

Heterogeneity

There are some differences between early and late retirees. An early retiree may not have a strong work history which could reduce their chances to receive benefits. Even those who were successful during their working years might not retire as young as their 65-year-old counterparts. These variations in the retirement age may be due heterogeneity in earnings. But the study's authors acknowledge the contributions of many people.

A study of net worth returns shows that heterogeneity is more common. The standard deviation for returns is 7.9%. The range of the 90th and tenth percentiles is 16.9%. These results indicate that returns to financial wealth are more diverse due to the cost of debt and leverage. The distribution of net worth returns is more uneven than the returns to net wealth. It also exhibits a greater degree of kurtosis and a longer tail to the left. Pearson's coefficient of skewness is -6.31.

Expectations and the impact of earnings

This research uses a new framework to measure lifetime earnings and compare them with Social Security benefits. This method is based on administrative records and measures lifetime earnings instead of Social Security earnings. Additionally, it represents trade-offs at several dimensions. These data are not limited to Social Security earnings. They can include uncovered earnings. As a result, these data provide a more accurate measure of lifetime earnings.

Social Security Administration (SSA), using CPS data, has shown that close to 90 percent of older households were able to receive Social Security income in any year since 1970. It varied in the amount of income received from that source between 66 and 84 per cent of total income. Poterba (2014) also used 2013 CPS data for total income levels. It found large variation in the proportion of households that receive Social Security income. This shows that earnings can have a significant impact on expectations of social security in both the long- and short-term.

The impact of early retirement

The topic of early retirement and the future of social security is controversial. Some research has indicated that younger people are more inclined to retire earlier. However, it remains to be seen if this will result either in fewer beneficiaries or more benefits. Researchers suggest that the workers' age limit for Social Security benefits could be lower to increase their entitlement to more money. But this idea isn't widely accepted.

In addition, claiming Social Security benefits early means that you will miss out on tax-advantaged savings opportunities. Early claimants will also have a lower base for COLA adjustments during retirement. This could be a problem in an era with high inflation. Consider how long you plan to live, and what kind of health care you'll need. When planning your retirement, it is important to consider the effect of early retirement on future Social Security.

FAQ

How does wealth management work?

Wealth Management is where you work with someone who will help you set goals and allocate resources to track your progress towards achieving them.

Wealth managers not only help you achieve your goals but also help plan for the future to avoid being caught off guard by unexpected events.

They can also prevent costly mistakes.

What is investment risk management?

Risk management is the act of assessing and mitigating potential losses. It involves the identification, measurement, monitoring, and control of risks.

Investment strategies must include risk management. The purpose of risk management, is to minimize loss and maximize return.

These are the key components of risk management

-

Identifying the sources of risk

-

Measuring and monitoring the risk

-

How to manage the risk

-

Manage your risk

Who should use a Wealth Manager

Anyone who wants to build their wealth needs to understand the risks involved.

New investors might not grasp the concept of risk. Bad investment decisions could lead to them losing money.

The same goes for people who are already wealthy. They may think they have enough money in their pockets to last them a lifetime. They could end up losing everything if they don't pay attention.

Everyone must take into account their individual circumstances before making a decision about whether to hire a wealth manager.

What are the potential benefits of wealth management

Wealth management's main benefit is the ability to have financial services available at any time. Savings for the future don't have a time limit. It also makes sense if you want to save money for a rainy day.

You can choose to invest your savings in different ways to get the most out of your money.

For example, you could put your money into bonds or shares to earn interest. You could also buy property to increase income.

You can use a wealth manager to look after your money. You won't need to worry about making sure your investments are safe.

What Are Some Benefits to Having a Financial Planner?

A financial plan will give you a roadmap to follow. You won't be left guessing as to what's going to happen next.

This gives you the peace of mind that you have a plan for dealing with any unexpected circumstances.

A financial plan can help you better manage your debt. You will be able to understand your debts and determine how much you can afford.

A financial plan can also protect your assets against being taken.

Which are the best strategies for building wealth?

Your most important task is to create an environment in which you can succeed. You don't want to have to go out and find the money for yourself. You'll be spending your time looking for ways of making money and not creating wealth if you're not careful.

You also want to avoid getting into debt. Although it is tempting to borrow money you should repay what you owe as soon possible.

You're setting yourself up to fail if you don't have enough money for your daily living expenses. Failure will mean that you won't have enough money to save for retirement.

Therefore, it is essential that you are able to afford enough money to live comfortably before you start accumulating money.

Statistics

- According to Indeed, the average salary for a wealth manager in the United States in 2022 was $79,395.6 (investopedia.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

External Links

How To

How to invest when you are retired

After they retire, most people have enough money that they can live comfortably. But how can they invest that money? While the most popular way to invest it is in savings accounts, there are many other options. You could sell your house, and use the money to purchase shares in companies you believe are likely to increase in value. You could also purchase life insurance and pass it on to your children or grandchildren.

You can make your retirement money last longer by investing in property. If you invest in property now, you could see a great return on your money later. Property prices tend to go up over time. Gold coins are another option if you worry about inflation. They don't lose their value like other assets, so it's less likely that they will fall in value during economic uncertainty.